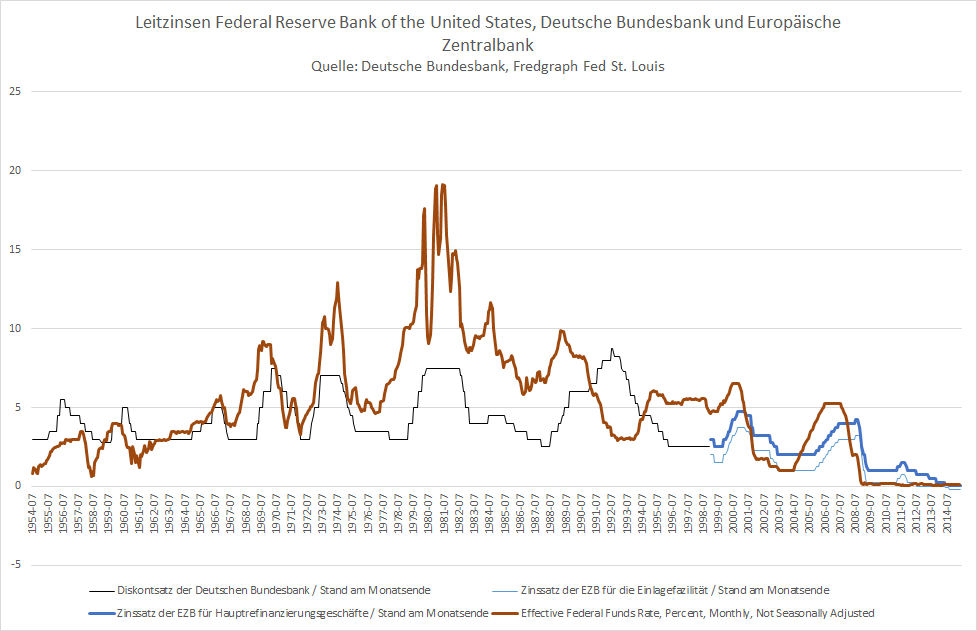

The other side of inflation is the interest rate policy of central banks. Interest rate policy or the key interest rate effectively controls the money supply. It determines how expensive it is to borrow money (as a bank or similar). The cheaper money is lent, the more people and institutions will take advantage of this opportunity. This increases the amount of money in circulation and as always in a market economy: when there is more of something, it becomes less valuable. Purchasing power decreases through higher prices and inflation accelerates. At least in theory. A great mystery of the time since the 2007 banking crisis remains that inflation does not rise sharply. Even though key interest rates are lower than ever before, and additionally central banks are massively distributing new money through bond purchases with freely printed money.

Interest rates: Downward for 40 years. Image: CC BY-SA 4.0, Link

To what extent the low inflation rates also correspond to reality or are rather due to strange baskets of goods and calculations, let that be left aside for now. In any case, according to official figures, we in the Western world are living in an environment of surprisingly low inflation – contrary to all expectations. Which is why central banks also have no urgent reason to significantly raise key interest rates. That in turn is good for stock markets. Even without rising inflation, stock prices are boosted by cheap money.

The calculation here is simple, but unfortunately only works well for the very rich: If stocks yield an average of around 7% per year and it only costs 2% per year to borrow money, then you would be stupid not to borrow money to invest it in stocks. This is a so-called carry trade. The lower the interest rates, the more profitable and thus attractive it becomes.

Money supply vs. stock price over the last 40 years (USA)

Ready for Better Investment Decisions?

Start your free trial today - stock analysis with artificial intelligence.

Full Transparency | Full Access | Cancel anytime

The same principle also applies to bonds. They become more desirable and their interest rates fall. This allows companies and states to borrow money more cheaply to finance expansion and investments, which is why hardly anyone has a great interest in rising interest rates. Except of course all those who have many savings in monetary form. Or until rising inflation forces a containment of the money supply. The situation has now become so absurd that bonds considered particularly safe, such as German government bonds, yield negative interest rates. In plain language, this means that when you buy German government bonds, you pay Germany for being allowed to lend them money. Specifically, you currently pay approximately 50 € for being allowed to lend Germany 1000 € for 10 years.

Rising key interest rates would therefore have drastic effects and rising inflation could force them. The attractiveness of the carry trade dissolves. Stocks are sold to repay the borrowed money. The market has been in an absolute growth environment over the last decade and was enthusiastic about the possibilities of mobility, e-commerce and entertainment. The funds from the carry trade therefore flowed primarily into the new giants: Facebook, Amazon, Netflix, Google (FANG) are the classic examples. Meanwhile, it has long since flowed into the entire tech sector and beyond. From cloud providers to hydrogen producers, they would all suffer disproportionately.

In the second step, problems would then arise for states. The higher the debt mountain, the more difficult refinancing becomes with rising interest rates. Because when the old bonds expire and the debts have not been reduced, they must be replaced by new ones at market prices. Interest payments therefore increase with rising interest rates in relation to the total outstanding debt, not just on newly borrowed money. High debt therefore leads to sharply rising interest payments, which in turn lead to deteriorating prospects for the state. This in turn leads to higher interest rates that the state must pay for fresh money. A vicious circle – which is why Germany's policy has so far absolutely rightly placed so much value on the debt brake. In order to remain as capable of action as possible in difficult times from Corona to hyperinflation.

Lars Wißler owns shares of Amazon and Alphabet (Google). PWP Leeway does not own any of the mentioned stocks.