Hello after a wild week. Right off the bat: I accompanied it extremely poorly in my assessment and commentary, which pains me. A brief review. For about a month now, we here at Leeway have been relatively permanently issuing warnings about market behavior because the market structure presented itself in a highly unpleasant manner.

Last week, on the night from Wednesday to Thursday, after the dynamic recovery from the previous week's low, I considered the dangerous phase to be over - on the last day of this phase when the market showed strength.

Why? One reason was sentiment: after investor sentiment was overheated and euphoric around the turn of the year, it had reversed course the week before and was clearly in pessimistic territory. Added to this was a long-term buy signal in market timing. In the long-term signal, such a signal ultimately means that the balance between purchases and sales on that day in market breadth is clearly shifted towards „buying“.

So there was enough fuel in the tank for a long-term movement (pessimistic sentiment), there was a clear thrust in the direction of a breakout (long-term buy signal), and the market had both reduced the overextension upwards (consolidated) and dynamically negated the previous weakness. In doing so, the price positioned itself above the large resistance area (red). Accordingly, my view was directed upwards.

S&P 500 Daily Candles

In retrospect, I should have waited for confirmation and the final breakout (above green) the following day, because the situation turned out to be a textbook bull trap (upper arrow). During the night of Thursday (lower arrow), the medium and short-term buy signals also became active, and since then we have been in a clear overextension situation. At least the Stock of the Week demonstrated the advantage of good entries through chart analysis and lost less than 1% compared to the 5 – 6% loss of the US market.

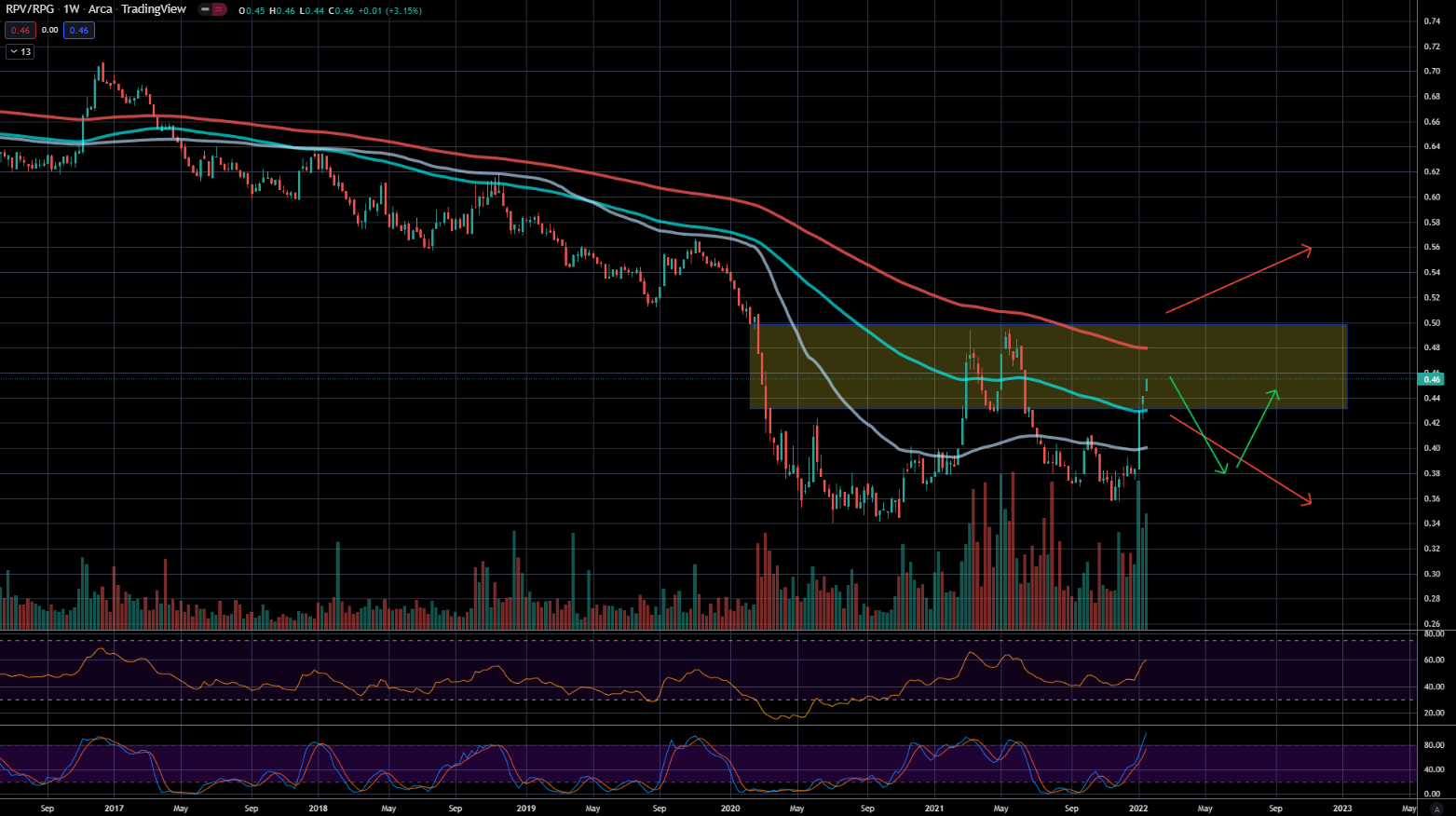

But enough of the past - let's look to the future. The first focus is the re-ignited topic of Value vs. Growth. Since the beginning of the year, we have seen a massive shift towards Value. We discussed this topic in the chat back in the old year and diversified portfolios towards Value. The subsequent movement was nonetheless unprecedented. However, the reallocation had begun much earlier, best seen in the chart of the ARK Innovation ETF.

ARK Innovation Daily Candles

ARK Innovation, the flagship fund of Cathy Woods and one of the most discussed funds of last year, had catapulted itself into the spotlight after Corona with a bet on the hottest hype companies, achieving an extreme return. Meanwhile, the fund has lost more than 50% of its value since its high in February. The last few weeks mark only the last drops of losses, certainly also triggered by the outflow of capital from the many copycat funds.

The flight from the Extreme Growth sector should end here for now. The crash was too extreme and the topic is now too media-accompanied. The rebalancing from the beginning of the year had brought momentum once again, which is now running out. Now is not the time in the short term to make the portfolio more defensive and Value-oriented. But another area was similarly overextended as the ARK Innovation universe: of course Crypto-Currencies. And there is still much room to fall here. The chart shows the Top 30 Global Cryptos. Not a pretty picture: the large head and shoulders pattern from August to January was triggered, as long as the price remains below the green line, there is still quite a bit ahead (or below) us. Target 6000 points, -60%.

Top 30 Crypto Basket

Looking somewhat further into the future, however, it should be very appropriate to continue orienting towards Value. Value doesn't necessarily have to mean boring. With our Value Screener one can easily find highly interesting stocks. How about a US semiconductor and chip company, a beneficiary of the chip shortage in a long-term uptrend, solid margins, debt of 35%, over 70% equity, almost 85 billion € market value, a P/E ratio of under 20 and price-to-book ratio less than 2? I will take a close look at Micron Technologies (ranked 3rd in US Tech in the Value ranking) when I think about Value. The downside risk is certainly smaller than with Nvidia and AMD.

Ready for Better Investment Decisions?

Start your free trial today - stock analysis with artificial intelligence.

Full Transparency | Full Access | Cancel anytime

Value vs. Growth long-term chart. Resistance area in yellow and preferred scenario are the green arrows.

Regarding the broader market: while Europe and especially Germany were able to hold up well, the American side, as already mentioned, had to give up drastically. Investor sentiment is consequently historically pessimistic and since Thursday we have been in a clear short-term downward overextension. Where we are here can be wonderfully seen with our newest feature. Daily we determine the historical points in time when the situation was most similar to the current one. I have compiled the five most similar time points.

Most Similar Time Points in the S&P 500. From top left to bottom right: 13.12.2021, 05.08.2019, 24.08.2015, 19.12.2018 and 19.10.2012.

These instances exactly match my personal assessment. We are at the end of a downward movement. Either we see here for a few days a very dynamic counter-movement that doesn't make it to new highs but instead must further digest this first shock. Or we slip through here once more (bottom left), then we are in truly extreme territory at the end of crash movements (like Christmas 2018) and could expect an upward movement lasting months.

I personally favor a mix of 2015 and 2012 (top right and bottom). First a dynamic counter-movement that ultimately fails, and then in about 2 weeks starting a second downward wave that takes us another 10% lower. That would then also complete the expected 20% correction this year. The European market will then probably not be able to escape this second wave either. In this context, another look at the Dollar Index DXY is important, which I had already focused on at the beginning of the month.

It shows strength again and could be gearing up to crack the important resistance at the previous year's highs. This behavior could well explain the relative weakness of the US markets compared to Europe. However, as already noted in the last commentary on the Dollar Index, a strong dollar has historically been a clearly negative factor for Europe and the Emerging Markets as well.

In short, I'm buying here to tend to exit the market in a few days to weeks with a few percent plus. And I'm overweighting aggressive Growth to increase the Value quota in a few weeks to months.

Good luck!

Lars