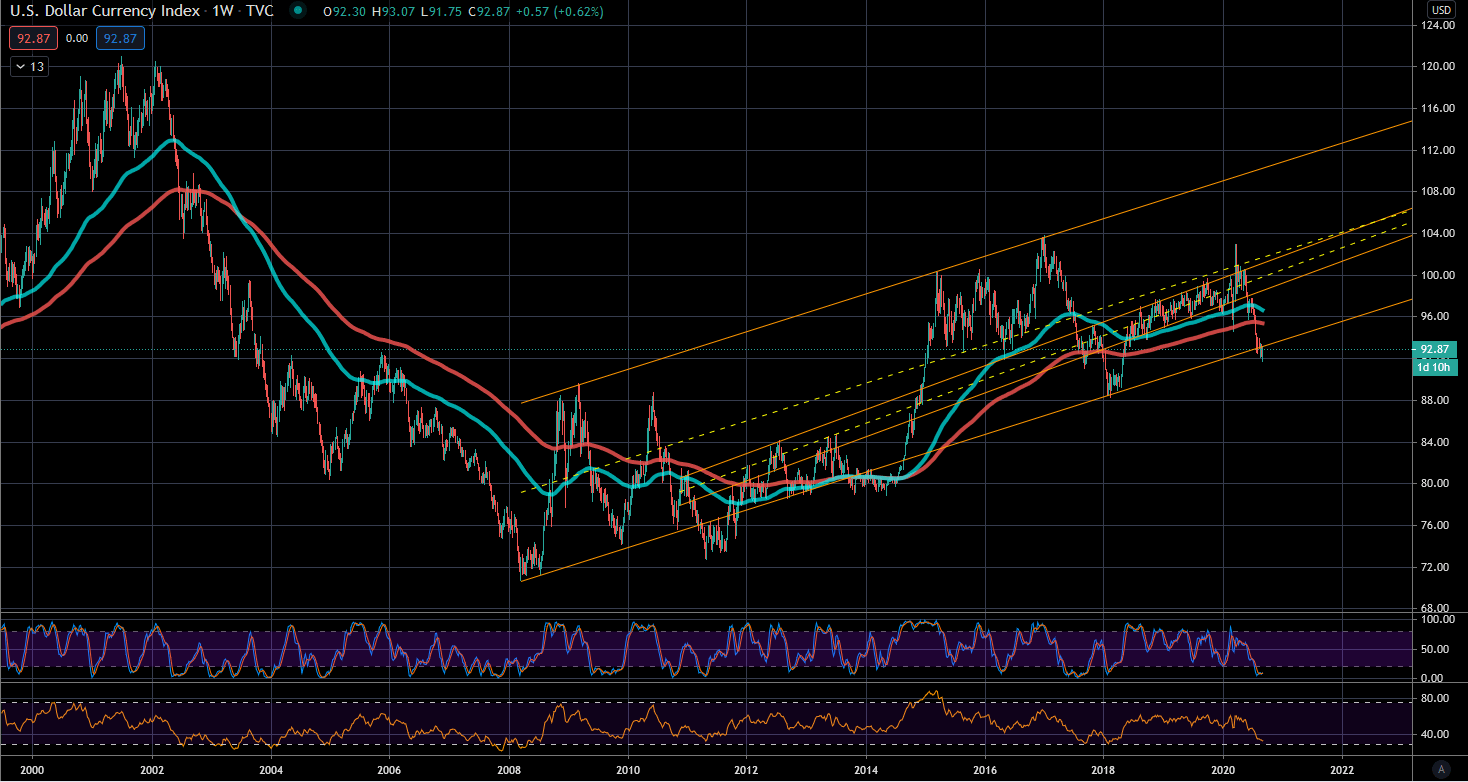

The Dollar Index DXY is a weighted basket of currency pairs that quite accurately reflects the value of the dollar compared to all other currencies. Since 2009, the dollar has been in a steady upward trend, particularly compared to the euro, from a peak of 1.50 $ per € to as low as 1.05 $ per €. This massively devalued our wealth in international comparison, and the outperformance of US stock markets seems all the more extreme, because the strong dollar actually worked against them. This trend could now reverse; the dollar is struggling very much at the lower end of the channel that defines the upward trend of the last decade.

The dollar exchange rate therefore has massive effects on the global economy. Capital flows toward weak currencies, which is why so many countries like China, Switzerland, or indeed the USA try to lower their exchange rate. Because with a low exchange rate, one's own products but also companies automatically become cheaper and thus more attractive from an international perspective. From a corporate perspective, those who produce in countries with the dollar as primary or secondary currency and sell to countries with a strong other currency, particularly Europe, benefit most. This description applies to American companies only secondarily. The emerging markets benefited most in the past. In these countries, the dollar is often a secondary currency or business currency to ensure stability, and the companies are agile and specialized enough to maximally profit from such currency advantages in purchasing and sales. The iShares MSCI Emerging Markets ETF (EEM) behaved almost like a mirror image to the dollar index over the last 15 years, and a falling dollar regularly led to significant price gains in this area.

Ready for Better Investment Decisions?

Start your free trial today - stock analysis with artificial intelligence.

Full Transparency | Full Access | Cancel anytime

A weak dollar is particularly problematic for companies that produce in countries with appreciating currencies but export internationally. So specifically European companies whose value creation takes place largely in Europe and whose costs do not mainly consist of imported goods (because those become cheaper for Europeans), but who generate significant portions of their profits abroad, will see the effects of a falling dollar in falling margins. In such situations, it is important to have generated high margins from the outset in order to be able to cushion such effects. No wonder that high margins, at least to a certain degree, repeatedly crystallize as one of the strongest indicators of rising prices.

In short: A low currency attracts manufacturing processes and thus labor, simplifies exports, and makes imports more expensive. One of the smartest investments for residents of regions with very strong currencies is to have work performed in countries with weak currencies. It's simply cheap. For export nations, a weak currency is therefore initially good. Things look somewhat different when considering debt or the ability to borrow money. A falling currency makes it harder to repay debts in foreign currencies, because the interest on, for example, a bond in euros will automatically increase from the perspective of a company or state operating in dollars. After all, one's own money is devalued compared to the money in which debts were incurred. Above all, however, it makes it harder to obtain new money, logically. It is fundamentally disadvantageous for Europeans to grant a loan in dollars, i.e., for example, to buy an American government bond, when a falling dollar is expected. Because the value of the bond and the interest payment are calculated in dollars and fall just as the dollar falls.

Whether the dollar will actually break downward is the question. Many are prophesying the great dollar crash. At the same time, Goldman Sachs recently announced they had closed their short positions in the dollar because it was extremely oversold. However, the first extremes in momentum are rarely the end of a movement; it usually has to dissipate first before it reverses, and Goldman (and others) like to say one thing to do another (more cheaply). Meanwhile, the volatility index VIX is rising significantly despite (dollar) stock markets at record levels. The reasons are nicely explained here. In short, the professionals are afraid of missing the rally but are also very uncertain, which is why they are disproportionately using options. This drives up the prices of options and thus also the VIX. Meanwhile, our purchase interest index continues to fall and yesterday reached a level for the first time that overall indicates clear selling interest. I can only continue to advise caution.